The report “Insulation Coating Materials Market by Type (Acrylic, Epoxy, Polyurethane, YSZ, and Mullite), End-Use Industry (Aerospace, Automotive, Marine, Industrial, Building & Construction), and Region - Global Forecast to 2023”, The insulation coating materials market size is estimated at USD 8.7 billion in 2018 and is projected to reach USD 12.5 billion by 2023, at a CAGR of 7.5% between 2018 and 2023. The increasingly stringent policies at workplace and increase in shipbuilding activities are expected to drive the insulation coating materials market.

In July 2018, AkzoNobel opened a new coatings facility in Kenya with warehousing for the company’s marine, protective, and powder coatings. This expansion will act as a gateway for the company to the entire East Africa.

In June 2017, The Sherwin-Williams Company acquired Valspar Corporation (US). According to Valspar, shareholders received USD 113 per share in cash. This has helped the company strengthen its brand portfolio and expand its product range and global footprint.

In July 2017, PPG acquired The Crown Group, a US-based coatings application services business, from High Road Capital Partners and Charter Oak Capital Partners. This acquisition will enhance PPG’s ability to cater to its customers, including OEM.

♠ Primary Research -

The insulation coating materials market comprises several stakeholders such as raw material suppliers, processors, end-product manufacturers, and regulatory organizations in the supply chain. The demand side of this market is characterized by the development of the construction, marine deck, aerospace, industrial, and automotive industries. The supply side is characterized by advancements in technology. Various primary sources from both the supply and demand sides of the market were interviewed to obtain qualitative and quantitative information.

What are your views on the growth prospects of the insulation coating materials market? What is the current scenario and how will it change in the future?

What is the estimated demand for insulation coating materials? Which type is used the most in the manufacturing of the same?

How are regulations affecting the insulation coating materials market? What are the different regulations that need to be followed in different regions?

What are the upcoming technologies/product areas that will have a significant impact on the market in the future?

What is the average price range for the different types of resins used in making of insulation coating materials? Does the pricing differ on the basis of end-use industry?

Contact: Mr. Aashish Mehra MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA : +1-888-600-6441 Email: newsletter@marketsandmarkets.com Visit Our Website: https://www.marketsandmarkets.com/

The use of carbon fiber prepreg is becoming crucial in aerospace & defense and automotive industries due to the increase in demand for high strength, operational stability at high temperatures, and lightweight materials. The carbon fiber prepreg market is projected to reach USD 11.5 billion by 2024, registering a CAGR of 10.5%, from 2019 to 2024.

In May 2017, Hexcel Corporation entered into an agreement with Irkut Corporation (Russia) for the supply of HexPly carbon fiber/epoxy prepreg for the MC-21-300 new generation commercial aircraft.

In March 2017, Solvay launched SolvaLite 730 prepreg for high volume automotive applications. It provides sub 60 seconds cure capability, exceptional toughness, and low tack. It is storage stable at room temperature.

In March 2017, Toray Industries, Inc. expanded its carbon fiber capacity at its Jalisco plant in Mexico. This expansion will support the company’s strategy of meeting the growing demand for prepreg for automotive and wind energy applications.

From 2014 to 2018, new product launch and expansion were the key strategies adopted by industry players to maintain growth in the global carbon fiber prepreg market. These strategies accounted for 24% and 22%, respectively, of the overall strategies adopted between 2014 and 2018. The market players concentrated mainly on consolidation through new product launch and expansion with the intention of increasing their market shares and enhancing their sustainability.

• Leading Key Players -

The major manufacturers profiled in this report are SGL Group (Wiesbaden, Germany), Gurit Holdings AG (Wattwil, Switzerland), Park Electrochemical Corporation (Melville, U.S.), Toray Industries (Tokyo, Japan), Teijin Limited (Osaka, Japan), Royal TenCate N.V. (Almeo, The Netherlands), Hexcel Corporation (Connecticut, US), Solvay (Brussels, Belgium), Mitsubishi Rayon Co. Ltd. (Tokyo, Japan), Axiom Materials (California, US), and others. These companies have adopted various organic and inorganic growth strategies such as new product launches, agreements, and expansions to expand their global presence and increase their penetration into the carbon fiber prepreg market.

Contact: Mr. Aashish Mehra MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA : +1-888-600-6441 Email: newsletter@marketsandmarkets.com Visit Our Website: https://www.marketsandmarkets.com/

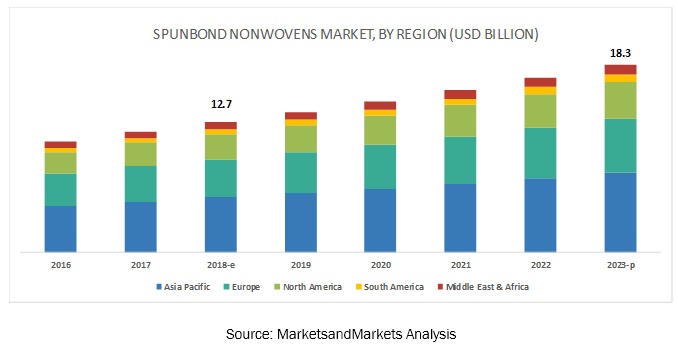

The spunbond nonwovens market is projected to grow from USD 12.7 billion in 2018 to USD 18.3 billion by 2023, at a Compound Annual Growth Rate (CAGR) of 7.6% during the forecast period.

The growth of the spunbond nonwovens market can be attributed to the increased consumption of spunbond nonwovens due to the growing population and demand for spunbond nonwovens from hygiene and medical segments.

♦ Leading Key Players Covered -

Schouw & Co. (Denmark), Mitsui Chemicals, Inc. (Japan), Johns Manville Corporation (US), Fitesa S.A. (Brazil), RadiciGroup SpA (Italy), Avgol Nonwovens (Israel), Kimberly-Clark Corporation (US), Berry Plastics Group, Inc. (US), Toray Industries, Inc. (Japan), Asahi Kasei Corporation (Japan), Pegas Nonwovens SA (Luxembourg), Kuraray Co., Ltd. (Japan), Kolon Industries, Inc. (South Korea), E. I. du Pont de Nemours and Company (US), and Mogul (Turkey). Total 25 major players covered.

♦ Recent Developments -

In February 2018, Fibertex Nonwovens acquired Brazilian nonwoven manufacturer DUCI, headquartered in Sao Paulo, which, in turn, helped gain a solid foothold in the South American market. With this acquisition, the company can realize the synergy created, as the acquired company has a strong product portfolio. It also helps the company enhance its geographical presence.

In May 2018, R2G Group, the owner of PF Nonwovens, acquired the operations of First Quality Nonwovens in the US and China. The production capacity of First Quality Nonwovens for spunbond nonwoven is 97000 tons in the US and 24000 tons in China. This strategic acquisition helped expand the presence of spunbond nonwoven business of PF Nonwovens in North America and Asia.

In November 2016, Asahi Kasei expanded its PP spunbond facility in Thailand by 20,000 tons per year due to the growing demand of PP spunbond in the country. This increased the facility’s total capacity to 60,000 tons per year.

The report “Medical Processing Seals Marketby Material ( Silicone, EPDM, Metals, PTFE, Nitrile Rubber), Type (O-Rings, Gaskets, Lip Seals), Application (Medical Equipment and Medical Devices), and Region - Global Forecast to 2023” The medical processing seals market is projected to grow from USD 1.4 billion in 2018 to USD 1.8 billion by 2023, at a CAGR of 5.0%. This growth is attributed to the increased demand for medical devices & equipment due to the growing healthcare industry. In addition, the expansion of the healthcare industry in APAC due to favorable trade policies proposed by the government of countries present in this region is expected to drive the medical processing seals market.

Silicone dominates the medical processing seals market and is projected to be the fastest-growing material segment

In terms of material, silicone accounted for the largest share of the market, globally. Silicone is highly preferred material for the medical sealing application, as it is highly compatible with human tissue and body fluids as compared to other elastomers. Also, silicone does not support bacteria growth which makes it highly suitable for devices that have close contact with the human body. Another important material used in medical devices is liquid silicone rubber (LSR). LSR is used in different critical medical applications such as cardiology, oncology, and orthopedics, and others.

O-rings dominate the medical processing seals market by type

O-rings are universally used in medical equipment & devices owing to their low cost. O-rings are used in different types of dynamic and static applications in the medical industry. Static applications such as fluid or gas sealing applications majorly consume O-rings. The increasing demand for devices and equipment such as drug delivery devices, valves, pumps, cylinders, connectors, fluid transfer devices, respiratory equipment, and dialysis equipment in the developing countries APAC, South America, and the Middle East & Africa is expected to drive the demand for medical processing seals.

North America is projected to be the largest medical processing seals market.

North America (comprising the US, Canada, and Mexico) is estimated to account for the largest share of the global medical processing seals market in 2018. Huge consumption and demand for new and innovative medical devices & equipment in the region due to the presence of a strong healthcare sector is driving the demand for medical processing seals in the region.

IDEX Corporation (US), Saint-Gobain S.A. (France), Freudenberg Group (Germany), Trelleborg AB (Sweden), Parker Hannifin Corp (US), Minnesota Rubber and Plastics (US), Marco Rubber & Plastic Products, LLC (US), Morgan Advanced Materials Plc (UK), Bal Seal Engineering, Inc. (US), and Techno AD Ltd (Israel) are the key players operating in the market.

In 2019, the silicone surfactants market is estimated at USD 2.0 billion and is projected to reach USD 2.5 billion by 2024, at a CAGR of 5.0% from 2019 to 2024. Rising demand for silicone surfactants from the end-use industries is expected to drive the silicone surfactants market.

Based on application, the emulsifiers segment is projected to lead the market, in terms of value, during the forecast period

The emulsifiers segment is estimated to lead the silicone surfactants market in 2019, due to rising demand for emulsifiers from the personal care, construction, and paints & coatings end-use industries. Increasing applications of emulsifiers in cosmetics and personal care products have also contributed to the growth of the emulsifiers segment. Emulsifiers are used to stabilize polyurethane foam; hence, the growth of polyurethane foam market is projected to fuel the growth of emulsifiers in the silicone surfactants market.

By end-use industry, in terms of value, the personal care industry is expected to lead the silicone surfactants market during the forecast period

Personal care, construction, textile, paints & coatings, agriculture are the major end-use industries for silicone surfactants market. The personal care segment is estimated to lead the silicone surfactants market in 2019, owing to increasing demand for silicone surfactants in applications such as skincare, haircare, and personal hygiene products. Rising demand for non-hazardous ingredients in personal care products is expected to fuel the growth of silicone surfactants in the personal care industry.

♦ Recent Developments -

In January 2019, AB Specialty Silicones opened a production facility in Waukegan, Illinois to further increases silicone business. The expansion is expected to help the company increase its production capacity and cater to the demands of customers.

In August 2019, Elkem acquired Basel Chemie, a Korean producer of specialty silicone gels for cosmetics and water repellents. This acquisition helped Elkem cater to a wide range of end-users.

In August 2017, Shin-Etsu Chemical planned to expand its silicones production capacity in the US. This expansion is expected to help the company cater to the increasing demand for silicone products in North America.

Others (Conditioners, Thickeners, and Demulsifiers)

On the basis of End-use Industry, the silicone surfactants market is segmented as follows:

Personal Care

Construction

Textile

Paints & Coatings

Agriculture

Others (Automotive, Oil & Gas, and Pulp & Paper)

♦ Leading Key Players -

Evonik Industries AG (Germany), Dow Corning Corporation (US), Momentive Performance Materials Inc. (US), Wacker Chemie AG (Germany), Innospec Inc. (US), Shin-Etsu Chemical Co., Ltd. (Japan), Siltech Corporation (Canada), Elé Corporation (US), Elkem ASA (France), Supreme Silicones (India), Silibase Silicone New Material Manufacturer Co., Ltd. (China), Jiangsu Maysta Chemical Co., Ltd. (China), Elkay Chemicals Pvt. Ltd. (India), Hangzhou Ruijiang Performance Material Science Co., Ltd. (China), Harcros Chemicals Inc. (US), and SST Australia Pty Ltd. (Australia), among others are the major players in the silicone surfactants market.

The report “Colorless Polyimide Films Market by Application (Flexible Displays, Flexible Printed Circuit Boards, Flexible Solar Cells, Lighting Equipment, Others), End-Use Industry (Electronics, Solar, Medical, Others), Region - Global Forecast to 2025”, The colorless polyimide films market is projected to grow from USD 22 million in 2020 to USD 379 million by 2025, at a CAGR of 76.0% from 2020 to 2025. The market growth is driven by the increasing demand for colorless polyimide films from applications such as flexible displays, flexible solar cells, and flexible printed circuit boards, among others.

In March 2019, SK Innovation Co., Ltd. announced the completion of its demo plant to produce FCW, with commercial production scheduled for 2020. The company aims to offer clear polyimide films to the global foldable smartphone market, which is expected to grow in the coming years.

In March 2019, Kaneka Corporation developed colorless polyimide films for flexible electroluminescent (EL) displays, with plans to start sample shipment by the first half of 2019. The company expects the market for colorless polyimide films to grow due to the emergence of next-generation electronic devices, which will result in increased demand for flexible displays.

Based on application, the colorless polyimide films market has been segmented into:

Flexible Displays

Flexible Printed Circuit Boards

Flexible Solar Cells

Lighting Equipment

Others (reflectors & connectors for space antennas and drug delivery tubes)

Based on end-use industry, the colorless polyimide films market has been segmented into:

Electronics

Solar

Medical

Others (aviation and space research)

♦ Speak To Analyst - https://www.marketsandmarkets.com/requestsampleNew.asp?id=16252223 ♦ Leading Key Players - Key players in this market are E. I. du Pont de Nemours and Company (US), Kaneka Corporation (Japan), Kolon Industries Inc. (South Korea), SK Innovation Co., Ltd. (South Korea), and Sumitomo Chemical Company Ltd. (Japan). Other noteworthy public and private players in this market are Wuhan Imide New Materials Technology Co., Ltd. (China), Industrial Summit Technology (Japan), NeXolve Holding Company (US), Wuxi Shunxuan New Materials Co., Ltd. (China), and Suzhou Kinyu Electronics Co., Ltd. (China).

Contact: Mr. Aashish Mehra MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA : +1-888-600-6441 Email: newsletter@marketsandmarkets.com Visit Our Website: https://www.marketsandmarkets.com/

The report “Engineered fluids (Fluorinated fluids) Market by Type (Lubricants, Solvents, Heat Transfer Fluids), End-Use Industry (Electronics & Semiconductor, Automotive, Chemical Processing, Oil & Gas, Power Generation, Aerospace), Region - Global Forecast to 2023” The engineered fluids (fluorinated fluids) market is estimated at USD 854 million in 2018 and is projected to reach USD 1,304 million by 2023, at a CAGR of 8.8% between 2018 and 2023. The versatility and superior properties of engineered fluids (fluorinated fluids) and increasing investments in APAC are expected to drive the market.

In February 2017, Chemours opened a new production facility at its Christi plant in Ingleside, Texas (US). This will triple the company’s capacity for the HFO-1234yf-based-products and make it a world leader in low global warming potential products.

In February 2017, Solvay acquired Energain Technology from DuPont, thereby, expanding its product portfolio catering to the battery production industry. This acquisition will boost Solvay’s technological road map in the battery production industry.

♦ Leading Key Players -

The leading players in the engineered fluids (fluorinated fluids) market are Daikin Industries (Japan), Solvay SA (Belgium), The Chemours Company (US), 3M (US), Asahi Glass Company (Japan), Halocarbon Products Corporation (US), Halopolymer (Russia), F2 Chemicals (UK), IKV Tribology (UK), Lubrilog Lubrication Engineering (France), Nye lubricants (US), and Interflon (Netherlands).

Browse 151 market data Tables and 34 Figures spread through 145 Pages and in-depth TOC on “Engineered fluids (Fluorinated fluids) Market by Type (Lubricants, Solvents, Heat Transfer Fluids), End-Use Industry (Electronics & Semiconductor, Automotive, Chemical Processing, Oil & Gas, Power Generation, Aerospace), Region - Global Forecast to 2023”

What are the global trends in demand for engineered fluids (fluorinated fluids)? Will the market witness an increase or decline in demand in the coming years?

What is the estimated demand for engineered fluids (fluorinated fluids)? Which type is used the most in the end-use industries?

What were the revenue pockets for the engineered fluids (fluorinated fluids) market in 2017?

What are the upcoming technologies/product areas that will have a significant impact on the market in the future?

Which are the major engineered fluids (fluorinated fluids) manufacturers, globally?

Contact: Mr. Aashish Mehra MarketsandMarkets™ INC.630 Dundee Road Suite 430 Northbrook, IL 60062 USA : +1-888-600-6441 Email: newsletter@marketsandmarkets.com Visit Our Website: https://www.marketsandmarkets.com/

The market for caprolactam is estimated to grow from USD 13.1 billion in 2018 to USD 15.6 billion by 2023, at a CAGR of 3.59% during the forecast period. The base year considered for this study is 2017 and the forecast period is from 2018 to 2023.

♦ Simply Download PDF Brochure - https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=108120798 In 2017, the caprolactam market in the nylon 6 fibers segment accounted for the largest share of 47.3%, in terms of volume, and is projected to register a CAGR of 2.90% between 2018 and 2023. The caprolactam market in the nylon 6 engineering plastics segment is projected to register a CAGR of 3.54%, in terms of value, between 2018 and 2023. The increasing demand for caprolactam in engineering plastics and films application is expected to drive the market for caprolactam. The high growth of the caprolactam market is primarily due to the growing electrical & electronics and automotive industries.

♦ Recent Developments -

In May 2018, Aquafil and Genomatica announced the formation of Project EFFECTIVE, a multi-company collaboration to produce more sustainable fibers and plastics for commercial use by using renewable feedstocks and bio-based technologies. One of the key objectives of Project EFFECTIVE is to develop a more sustainable nylon, made from bio-based caprolactam produced using renewable feedstocks.

In February 2018, Aquafil signed an agreement with INVISTA, one of the world’s largest integrated producers of chemical intermediates, polymers, and fibers, to acquire certain tangible and intangible assets related to INVISTA’s nylon 6 business activity in APAC. This will accelerate Aquafil’s investment program in APAC, which has the highest potential, in terms of demand growth for synthetic fibers.

Contact: Mr. Aashish Mehra MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA : +1-888-600-6441 Email: newsletter@marketsandmarkets.com Visit Our Website: https://www.marketsandmarkets.com/

The global automotive headliner market size is projected to grow from USD 16.6 billion in 2020 to USD 20.4 billion by 2025, at a CAGR of 4.2%, during the forecast period. The increase in demand for advanced headliners in premium segment vehicles, rising demand for interior styling, perceived quality, and convenience features, and government regulation for lightweight and safety are driving the automotive headliner industry growth.

♦ Key Market Players -

Grupo Antolin-Irausa, S.A. (Spain), Motus Integrated Technologies (US), Toyota Boshoku Corporation (Japan), Kasai North America, Inc. (US), International Automotive Components Group SA (Luxembourg), Howa Co., Ltd. (Japan), UGN, Inc. (US), SA Automotive (US), Hayashi Telempu Corporation (Japan), Freudenberg Performance Materials (France), Inteva Products, LLC (US), and IMR-Industrialesud Spa (Italy) are some of the players operating in the global automotive headliner market.

In April 2018, Grupo Antolin opened a manufacturing facility in Alabama, US, for the production of automobile interiors, including doors, headliners, lighting fixtures, cockpits, and trim. Through this, Grupo Antolin joined a dynamic and expanding auto sector in Alabama, which includes three assembly plants, an engine plant, and a broad-based network of suppliers.

In August 2019, Motus Integrated acquired Janesville Fiber Solutions, which provides high-performance engineered acoustical and thermal fiber automotive solutions. Through this, Motus strengthened its geographic footprint and its product portfolio.

The passenger vehicle segment is projected to be the fastest-growing vehicle type in the market during the forecast period.

The passenger vehicle segment dominated the overall automotive headliner market in 2019. The market in this segment is driven by the increase in demand for interior components in passenger vehicles. Additionally, the safety regulations in passenger vehicles are more stringent as compared to commercial vehicles. These factors are responsible for the growth of the passenger vehicle segment.

Contact: Mr. Aashish Mehra MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA : +1-888-600-6441 Email: newsletter@marketsandmarkets.com Visit Our Website: https://www.marketsandmarkets.com/